North American machinery shipment value dropped in second quarter, report says

Canadian Plastics

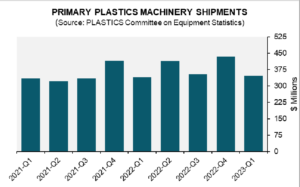

Market Forecast Plastics ProcessesAnd the value of second quarter shipments of injection molding and extrusion equipment dropped almost 20 per cent compared with a year ago.

Image Credit: Plastics Industry Association

The value of second quarter shipments of injection molding and extrusion equipment North America in the second quarter of 2023 was US$331.6 million, reflecting a decrease of 4.1% in comparison to the previous quarter, and a drop of 19.8% compared to last year.

These latest figures are from a new report from the Washington, D.C.-based Plastics Industry Association’s Committee on Equipment Statistics (CES).

Among the primary types of plastics machinery, the shipments of single-screw extruders demonstrated a “notable surge” of 39.3% in a quarter-over-quarter (Q/Q) analysis and exhibited an even more remarkable increase of 40.9% year-over-year (Y/Y), the report said. In contrast, shipments of twin-screw extruders experienced significant declines of 15.0% Q/Q and 11.2% Y/Y. Moreover, the shipments of injection molding machinery, which encountered a decline of 6.1% Q/Q, underwent an even more substantial decrease of 23.6% when observed on a year-over-year (Y/Y) basis.

“The manufacturing sector is the main customer of the plastics industry,” Perc Pineda, chief economist at Plastics Industry Association. “Although the U.S. economy exhibited resilience in the first half of 2023, the decline in plastics machinery shipments signifies a subdued manufacturing landscape.” Notably, Pineda said, the upswing in personal consumption expenditures (PCE) that followed the conclusion of the COVID-19 recession reached its peak in the first quarter of 2021, subsequently maintaining a consistent trajectory. “Interestingly, PCE on services commenced its recovery at a slower pace post-COVID-19 recession, and this upward trend has persevered, playing a pivotal role in driving the economic expansion in the first half of the year,” Pineda said.

During the second quarter, U.S. exports of plastics machinery saw a notable uptick of 10.2%, reaching a total value of US$252.8 million. The prime export destinations for U.S. plastics machinery, Mexico, and Canada, continued to hold their positions, collectively receiving exports worth US$126.4 million. This accounts for half of the entire U.S. plastics machinery export value. Conversely, imports experienced a decline of 10.5%, valued at US$458.6 million. As a result, the trade deficit in plastics equipment shrank by 32.0%, now standing at US$205.8 million.

In the most recent quarterly survey conducted by CES among plastics machinery suppliers to gauge their outlook on market conditions and equipment expectations, the results indicated a rise in participants anticipating an improvement in market conditions over the next twelve months compared to the previous year. The percentage of those expecting conditions to either remain the same or improve rose to 46.0%.

“As the economy readjusts, the shift between goods and services consumption is underway,” Pineda said. “However, sustaining a robust economic expansion, given a 5.5% benchmark interest rate or possibly higher in 2023, appears unlikely. The reliance on household debt for consumption raises concerns, particularly with the resurgence of student loan payments in September. This has the potential to adversely affect consumer spending and subsequently impact the plastics industry.” Global economic conditions and structural limitations in the U.S., such as labour supply, also play pivotal roles, Pineda said, and the German recession, European Union slowdown, and China’s economic deceleration are poised to influence the U.S. economy’s output, including the plastics sector.